Team Members: Bryce Tyler, Carter Schmitt, Mia Alex, Tianyou Tu, Yaxun Chen

Sponsor: MathWorks | Instructors: Ajay Anand, Ph.D. Cantay Caliskan, Ph.D.

Abstract: The FOMC, or Federal Open Market Committee, gathers eight times a year to set U.S. monetary policy, primarily deciding whether to raise, lower, or hold interest rates steady to manage inflation and support economic growth. These meetings result in policy statements that shift financial markets, affecting borrowing costs for consumers and businesses.

This project develops a framework for portfolio optimization that combines traditional quantitative financial modelling with textual signals extracted from Federal Open Market Committee meeting minutes. It incorporates daily S&P 500 stock pricing data, trading volume, and macroeconomic indicators such as the CPI, the 10-Year Treasury Yield, and the Federal Funds Rate. The minutes from the FOMC meetings were collected using Scrapy and transformed into structured numerical features using LLM-based prompt extraction using Ollama and the OpenAI API. The features capture policy tone, macroeconomic outlook, rate, and balance-sheet signals, uncertainty, topic patterns, keyword relevance, semantic shifts, and timing effects around FOMC meetings.

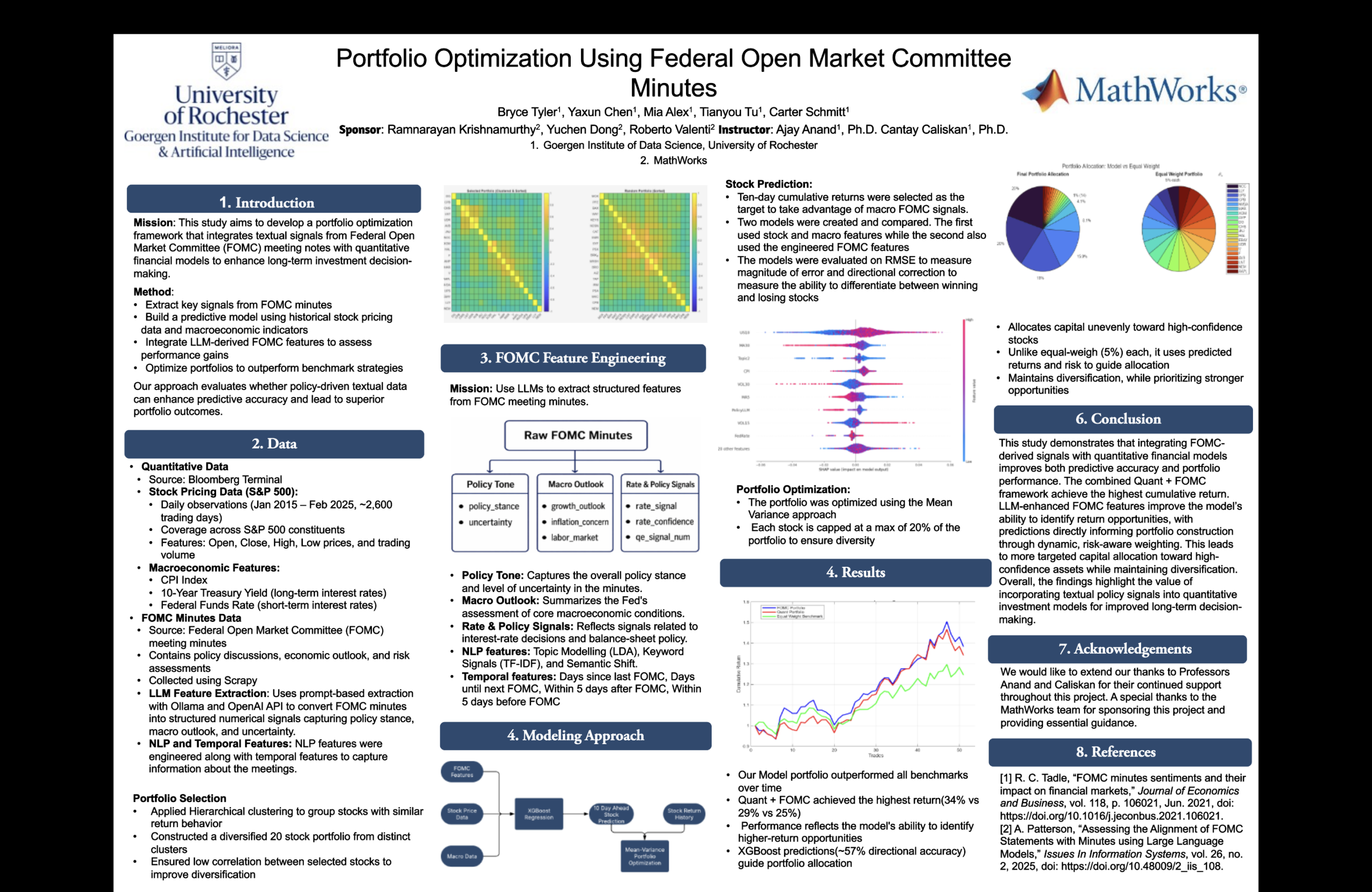

The framework developed evaluates whether textual information about economic policy can help improve stock return prediction as well as portfolio performance. The stocks were first grouped using hierarchical clustering in order to identify assets with similar return behaviour. Using this, a diversified stock portfolio containing 20 stocks with lower cross-correlation was created. The predictive models were trained to forecast ten-day cumulative returns. Upon comparing the baseline model that contained stock data and macroeconomic features against the enhanced model that also included FOMC signals, the predictions were evaluated using RMSE and directional accuracy. This Quant + FOMC model achieved approximately 57% directional accuracy, outperforming the benchmark.

Portfolio allocation was optimized with a mean-variance approach. To preserve diversification, each stock was capped to 20% of the portfolio. The optimized strategy placed more capital towards higher-confidence opportunities according to predicted returns and risk, compared to an equal-weight portfolio. The Quantitative + FOMC portfolio delivered the best cumulative return, topping the benchmark portfolios with returns of 34% versus 29% (Quant only) and 25% (FOMC only). Overall, the results suggest that incorporating LLM-enhanced FOMC signals into quantitative investment models can enhance predictive accuracy, allow for more targeted capital allocation, and improve long-term portfolio decision-making.

References: [1] R. C. Tadle, “FOMC minutes sentiments and theirimpact on financial markets,” Journal of Economicsand Business, vol. 118, p. 106021, Jun. 2021, doi:https://doi.org/10.1016/j.jeconbus.2021.106021.

[2] A. Patterson, “Assessing the Alignment of FOMCStatements with Minutes using Large LanguageModels,” Issues In Information Systems, vol. 26, no.2, 2025, doi: https://doi.org/10.48009/2_iis_108.